In this month’s market insights, we review August’s Jackson Hole gathering of central bankers

This year’s Jackson Hole symposium was focusing on “Structural shifts in the Global Economy”, and we highlight the five key takeaways from an investor’s point of view.

Whilst central bankers had the opportunity to interact amongst themselves during the usual annual gathering at Jackson Hole, there were also media interactions, with the market aiming to interpret some of the comments made by key central bankers.

There was something for both bulls and bears in terms of monetary policy comments. Our five key take-always from an investment point of view are summarised below, with more details in the report:

5 key take-always for investors from the Jackson Hole gathering:

- We are now in reactive monetary policy mode: Central bankers have shifted into data dependency, so their next interest rate moves will be determined by various data points they deem to be relevant in predicting inflation.

- Data dependency mode will bring higher market volatility: We expect more elevated volatility, as market participants guess and debate which data might be relevant to pay attention to, and in turn react.

- Central bank models are being challenged, which exacerbates volatility: Central bankers are acknowledging the limitations of their existing economic models, which further exacerbates unpredictability, and will therefore likely further fuel market volatility.

- Hawks focusing on elevated inflation comments: Hawks will focus on central bankers’ comments that relate to more work still needing to be done to tackle the elevated inflation levels.

- Doves focusing on comments around restrictive policies: Doves will focus on Jay Powell’s (Chairman of the US Federal Reserve) comment that interest rates have now moved to a level that is well above neutral, pointing to a restrictive monetary policy, and therefore speculating that we might have reached the end of the hiking cycle.

Our conclusions:

- We are closer to the end of the hiking cycle, which in our view should be more supportive for Quality Growth stocks.

- We expect an end to the hiking cycle by the end of this year, with potentially only 0-2 more hikes to come from both the US Federal Reserve (Fed) and the European Central Bank (ECB).

- Market expectations of a rapid pivot towards interest rate cuts in H1 2024 is premature however, given what we believe will be stickier inflation – we do not expect a pivot by key central banks until H2 2024.

- As flagged in our mid-year update, the divergence in monetary policies between western Central Banks, and some Asian/ emerging market (EM) central banks could become more apparent over the next six months. Western central banks will likely delay pivoting until H2 2024, while some of the Asian/EM Central Banks are already pivoting.

-

We maintain our view that inflation could end up being stickier than the market expects, and therefore central banks might be slow to reverse the hiking cycle.

Central bankers have moved into data-dependency, as they stated both prior and during the gathering. This is likely to mean that further hikes will be dependent on the various data points that will come out, specifically those they deem to be relevant to their so-called “inflation watching”. Whilst this doesn’t mean that all data will be relevant to their reflections on the next steps to take in terms of monetary action, it will lead to a higher degree of market volatility. This is because investors and market commentators will speculate on which data is both relevant, and the important focal point.

At the same time, inflation remains the more important focus for all central bankers, away from economic growth, with many views being expressed in the past that it is easier to reignite some growth, than to extinguish inflation if it becomes a more structural phenomenon. As such, it is likely that central banks will remain vigilant, and less willing to reverse course too rapidly in our view.

We maintain our view that inflation could end up being stickier than the market expects, and therefore central banks might be slow to reverse the hiking cycle. Whilst we are likely to see a deceleration in inflationary pressures in H2, notably as a result of the elevated base effect of last year, we do not share the market view that central banks will pivot rapidly in H1 2024.

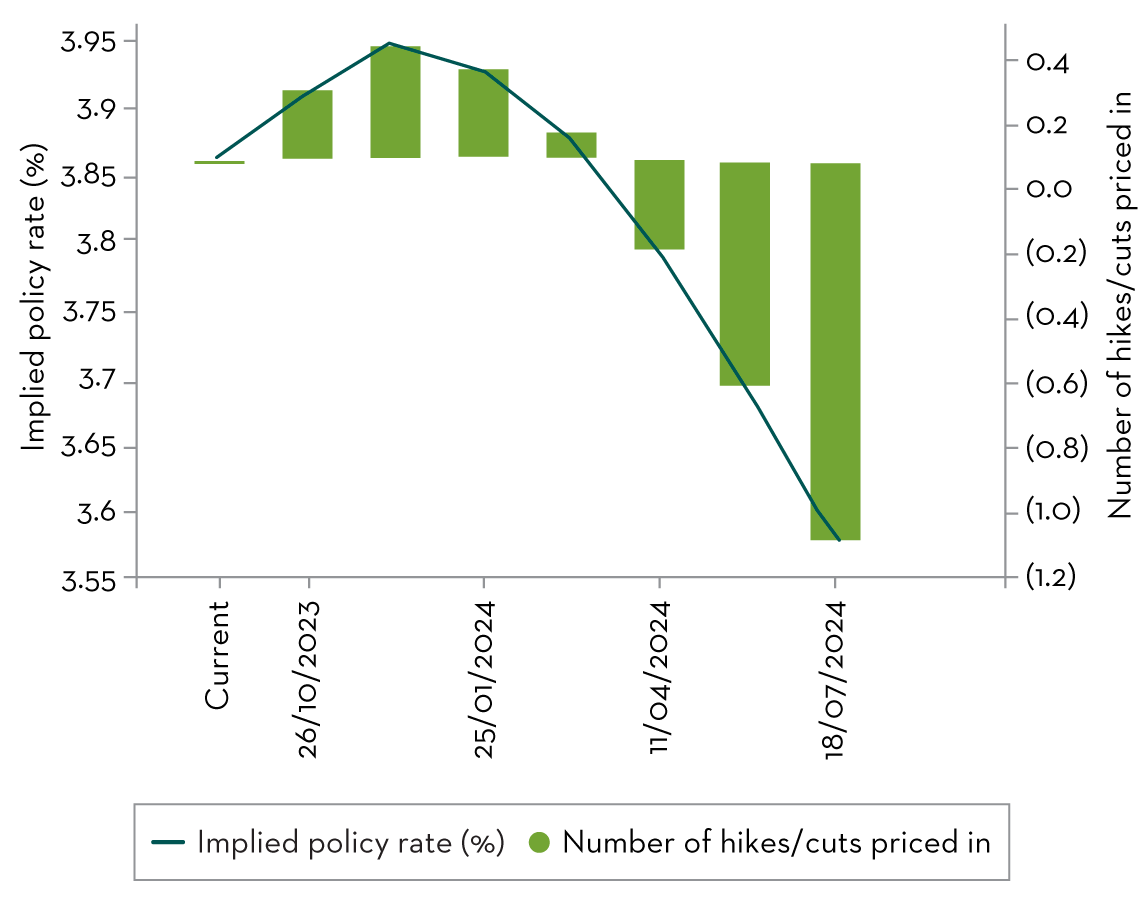

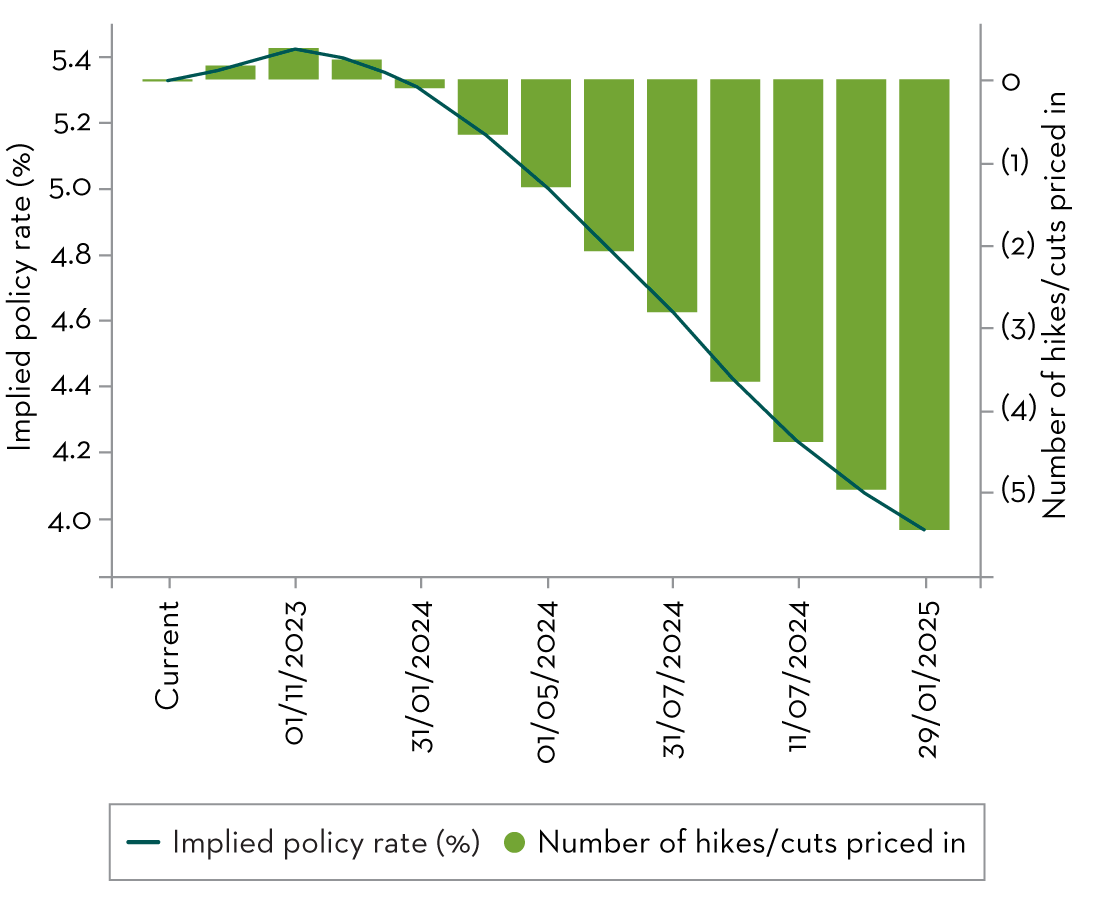

The charts below show the current market expectations of interest rate hikes/cuts for the Fed and the ECB. We might be nearing the end of the hiking cycle, but a pivot might take longer than current market expectations predict. This debate around when and how rapidly will central banks pivot will remain important for the market and for shorter term market participants. Fuelling further volatility, with each macroeconomic and microeconomic data point that might be deemed to be relevant.

Central bank policy rates versus rate hikes/cuts

European Central Bank

US Federal Reserve

Source: Bloomberg, September 2023.

On the margin, at the Jackson Hole gathering, Jay Powell sounded a bit more hawkish about prospects for inflation in the nearer term. Although he seemed to also have an eye on the long end of the yield curve, through a comment that real rates were “well above neutral levels now” (something that he swiftly acknowledged as not being a reliable estimate). This might be an important point to focus on, as it is the first time that Powell has explicitly acknowledged that monetary policy is now restrictive. He did emphasise that the Fed intends to “hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective”. He used the word “restrictive” when describing current monetary policies on a more than few occasions in his speech – in fact, the word was mentioned seven times in his approximately eight minute address.

Christine Lagarde (President of the European Central Bank) remained hawkish in her tone too, whilst also acknowledging that there is a shift to data dependency. She mentioned that progress is being made on the inflation front, but added that “the fight against inflation is not yet won”. She also flagged that there are concerns around a tight labour market raising more risks of persistence in inflation, flagging that “a surge in inflation can trigger catch up wage growth which can lead to a more persistent inflation process”; this is in line with our conclusion from our report back in October 2022, entitled “All eyes on wage inflation”. Given the ECB’s sole focus, as part of her mandate on inflation, and given the elevated inflation level, it is perhaps not a surprise that Christine Lagarde only mentioned the word “restrictive” once in her speech, which could be pointing to a more hawkish stance.

In fact, as time of writing this report the ECB raised rates by a further 25bps at its September meeting to 4.5%.

Other points that came out of the Jackson Hole gathering include:

Central bankers are questioning the economic models used by central banks for predicting outcomes:

- “Navigating by the stars under cloudy skies” – Jay Powell

- “Past regularities may no longer be a good guide for how the economy works” – Christine Lagarde

- “Policy making in an age of shifts and breaks requires an open mind and a willingness to adjust our analytical frameworks in real-time to new developments” – Christine Lagarde

Tight labour market raises risks of persistence in inflation:

- “A surge in inflation can trigger catch up wage growth which can lead to a more persistent inflation process” – Christine Lagarde

Ongoing elevated inflation, interest rates remaining higher for longer than expectations, and a more volatile market environment, has reinforced our conviction in the type of companies that investors should continue to focus on. These have the following characteristics:

- Earnings resilience, given the ongoing risk of earnings downgrades

- Pricing power, given the elevated and stickier inflation

- Balance sheet strength, given the higher interest rates environment

- Structural growth prospects, given that higher rates is likely to lead to a lower economic growth

We covered the importance of pricing power in an elevated and stickier inflation environment in a recent report. Here we discussed how to assess pricing power in a company, the systematic fields that we research as part of that, and we compared our strategies’ pricing power to the broader market, using gross margins trends as an indication of pricing power. Our readers can find the link to the report here.

Important Information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.

- Emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. Accordingly, investment in emerging markets is generally characterised by higher levels of risk than investment in fully developed markets.

- The strategy may invest in derivatives Index futures and FX forwards to obtain, increase or reduce exposure to underlying assets. The use of derivatives may result in greater fluctuations of returns due to the value of the derivative not moving in line with the underlying asset. Certain types of derivatives can be difficult to purchase or sell in certain market conditions.

For wholesale investors in Australia:

This material is provided on the basis that you are a wholesale client within the definition of ASIC Class Order 03/1099. MCIM is authorised and regulated by the FCA under UK laws, which differ from Australian laws.

For professional investors in Canada.

This material is intended for residents in, or incorporated in, Canada and are a Permitted Client for the purposes of MI 31-103. The information on this section of the website is not intended for use by any other person, including members of the public.

Martin Currie Inc, incorporated in New York with its registered office at 280 Park Avenue, New York, NY 10017 and having a UK branch registered in Scotland (no SF000300), Head office, 5 Morrison Street, 2nd floor, Edinburgh, EH3 8BH, Tel: +44 (0) 131 229 5252 Fax: +44 (0) 131 222 2532 www.martincurrie.com, operates under the International Adviser Exemption with the Ontario Securities Commission (‘OSC’) and is therefore currently not required to be registered as a portfolio manager for the purposes of MI 31-103. Martin Currie Inc. is also authorised by the UK Financial Conduct Authority.

For the avoidance of doubt, nothing excludes, limits or restricts our obligations to you under the UK Financial Services and Market Act 2000, National Instruments or any other applicable law or regulation.

The opinions and views in this website do not take into account your individual circumstances, objectives, or needs and are not intended to be recommendations of particular financial instruments or strategies to you.

This website does not identify all the risks (direct or indirect) or other considerations which might be material to you when entering any financial transaction. You should consult with your professional advisers before undertaking any investment activity. The information provided on this website should not be treated as advice or a recommendation to buy or sell any particular security or other investment. The information on this website has not been reviewed by any competent regulatory authority.

For professional investors:

In the People’s Republic of China:

This document does not constitute a public offer of the strategy, whether by sale or subscription, in the People’s Republic of China (the “PRC”). These strategies are not being offered or sold directly or indirectly in the PRC to or for the benefit of, legal or natural persons of the PRC.

Further, no legal or natural persons of the PRC may directly or indirectly purchase any of the strategy or any beneficial interest therein without obtaining all prior PRC’s governmental approvals that are required, whether statutorily or otherwise. Persons who come into possession of this document are required by the issuer and its representatives to observe these restrictions.

In Hong Kong:

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

In South Korea:

This document is for information purposes only. It is prepared and presented to provide an introduction to the business of MCIM and its related companies (collectively known as ‘Martin Currie’). This document does not constitute an offer to sell or a solicitation of any offer to invest in any security, fund or other vehicle managed or advised by Martin Currie.

None of the security(ies), fund(s) or vehicle(s) managed by or advised by Martin Currie are registered in South Korea under the Financial Investment Services and Capital Markets Act of Korea and accordingly, none of these instruments nor any interest therein may be offered, sold or delivered, or offered or sold to any person for re-offering or resale, directly or indirectly, in South Korea or to any resident of South Korea except pursuant to applicable laws and regulations of South Korea.

Martin Currie is not registered with or regulated by any regulatory authorities in South Korea.