Key Highlights

- Historically, long-run returns for this cohort have been impressive versus other market capitalisations

- Our UK smaller companies strategy considers the sweet spot for small cap investing to be companies with a market cap of between £100m and £1bn.

- Lower levels of analyst coverage provide opportunities for active managers

- And, why we have avoided ‘fallen angels’

UK Smaller companies have historically generated greater returns

The ‘Numis Indices 2022 Annual Review’ shows that smaller businesses in the UK have generated greater returns over the long run. While it’s not possible to invest directly in an index and any gains would not include fees, expenses, or sales charges, the Numis Smaller Companies Index (Ex IT’s) (NSCI) has advanced by 8,326% since 1955. This is the same as a 14.2% annual increase over the period and beats the Numis mid cap index by 1.4% per year (12.8% per annum). This empirical research also demonstrates that the greatest returns for UK equity asset classes have been delivered by companies valued in the bottom 2% of UK equity market capitalisation. Please see figure 1 below.

Why our ‘sweet spot’ is 100m-£1bn

In the Martin Currie UK Smaller Companies strategy, we maintain a disciplined focus on companies within a market capitalisation range between £100m and £1bn, our definition of small cap. This provides investors clear differentiation between our small- and mid-cap offerings but there are also some compelling reasons to hunt within this range including: impressive long run returns versus other market capitalisations and the fact that lower levels of analyst research present opportunities for active managers.

The NSCI is our benchmark and the latest rebalance cuts off at companies valued at £1.6bn and above. Historically, returns have diminished as one ascends the capitalisation spectrum so if we were to move up the market cap range, we would be broadening our universe to those businesses that have historically generated lower returns. Even taking into consideration the possibility of heightened volatility lower down the market cap scale, this is one of the reasons that we prefer to stick within our £100m to £1bn market cap range.

Whilst no universal definition exists, we believe that businesses valued above £1bn are not ‘small cap’ in terms of business size and maturity. As our strategy has a specialist small cap mandate, we believe that it would be inappropriate to add new portfolio businesses that we do not define as small cap.

Whilst no universal definition exists, we believe that businesses valued above £1bn are not ‘small cap’ in terms of business size and maturity.

Source: Numis Indices 2022 annual review

On the flip side, if we were to begin looking at companies with a market cap below £100m, we think liquidity becomes a concern and could impact our ability to buy or sell positions. We therefore define these companies as micro cap.

At the beginning of April, the median market capitalisation of the Martin Currie UK Smaller Companies portfolio is £392m and 88% of the portfolio assets were valued below £1bn. Those valued above £1bn were first bought when they were valued below our £1bn threshold and have since grown to exceed it.

We believe that this market cap profile healthily aligns to the areas of the market that have been most successful over the last 67 years.

According to the Numis indices 2022 annual review, the greatest returns over this period have been generated by companies that have sat in the bottom 2% of UK market capitalisation, which is currently around £400m and below There are risks with all investment, and this market cap range in particular includes risks of high volatility and liquidity.

The greatest returns over this period have been generated by companies that have sat in the bottom 2% of UK market capitalisation.

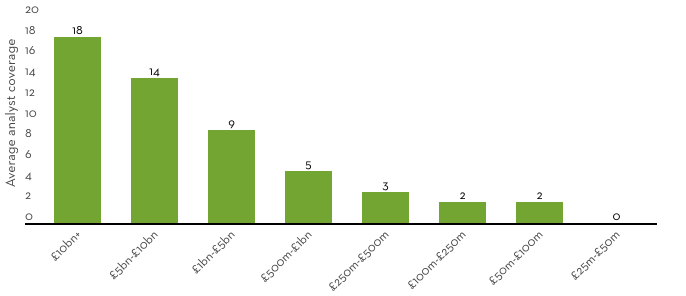

Diminishing sell-side coverage presents opportunities

We believe that the smaller the company, the likelihood of asset mispricing increases. One reason behind this is the MiFID II overhaul on permissible sell-side research activity, which has seen broker research coverage of smaller companies narrowing from both a quantity and quality perspective.

The chart to the left shows the average number of analysts covering each market capitalisation band. Five years ago, 11 analysts on average covered £500m-£1bn market cap names. This has now reduced to five and this trend continues as you move down the market cap scale.

With less coverage amongst these smaller names, market inefficiencies arise and create better opportunities for market mispricing that can be exploited by active fund managers.

Source: Numis Securities Research, as at 31 December 2022.

The index is annually rebalanced but we have avoided ‘fallen angels’

The benchmark for our UK smaller companies strategy is the Numis Smaller Companies Index (NSCI), which is rebalanced on an annual basis to reflect the lowest 10% of market capitalisation within the UK stock market. At the start of 2023, this meant the largest company in the index had a market cap of £1.6bn.

2022 was a strong relative year for the UK in general but much of this performance was driven by a small cohort of just 25 FTSE 100 businesses.

These mega cap companies were typically resource heavy giants in their respective fields. However, this narrow performance led to some significant shifts in index construction throughout the UK. As a result, many businesses dropped into the mid cap index from the large cap space, and into the smaller companies index from the mid cap space. Businesses that have been downgraded from a larger index to a smaller index are typically referred to as fallen angels.

The high levels of volatility have led to 29 of these ‘fallen angels’ making up 26% of the 2023 NSCI market cap – this is the highest ever and is over double the previous year. The impact that this has is profound – typically these businesses are not highly rated by the market and this has resulted in a significant de-rating of the index given their relatively large index weighting.

The price to earnings ratio (PE) of the NSCI dropped from 10x at the end of 2022 to 8.1x at the beginning of 2023. Along with an accompanying rising dividend yield, the fallen angels effect has significantly tilted the index towards value and against momentum factors. This has generated headwinds for the performance of our core/growth investment style, which has underperformed the index as value has performed well.

In addition, we find many of these fallen angels unattractive on a fundamental basis as they fail to meet our quality criteria. For example, one strong performer year-to-date is 7x leveraged. We would not consider a business this indebted as investable, irrespective of its size.

If we analyse the historic effect of buying fallen angels vs ignoring them since 1955, on average owning the fallen angels within the index has detracted from annual returns by 0.1%1 .

Offering investors a clearly defined UK small cap opportunity

We remain conscious of size/style drift at all times and our disciplined focus means we will not deviate from this in pursuit of short-term opportunity.

The FTSE 250 is broadly considered the proxy for UK mid cap businesses and the median market capitalisation of this index is £1.1bn (£1.9bn if we exclude investment trusts).

Inevitably, there is some crossover between the NSCI and the FTSE 250. However, we believe that by focussing our efforts on companies valued between £100m and £1bn, we are investing in the areas of the market that have historically generated the greatest returns. Consequently, we are offering a clear-cut UK smaller companies strategy to investors.

Regulatory information and risk warnings

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

This document is intended only for a wholesale, institutional or otherwise professional audience. Martin Currie Investment Management Limited does not intend for this document to be issued to any other audience and it should not be made available to any person who does not meet this criteria. Martin Currie accepts no responsibility for dissemination of this document to a person who does not fit this criteria.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

Please note the information within this report has been produced internally using unaudited data and has not been independently verified. Whilst every effort has been made to ensure its accuracy, no guarantee can be given.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.