Year to date performance

2022 has delivered a barrage of tumult the world over. As the globe recovers from the most severe pandemic endured in recent years, investors find themselves balancing soaring inflation with hawkish monetary policy amid a distinct style;rotation favouring defensive and value sectors, exacerbated by Russia’s invasion of Ukraine and subsequent global supply restrictions. The impact to global markets has been severe; the MSCI World Index has plummeted by over 15% year-to-date (YTD). Conversely, the previously unloved UK market has surfaced as a global leader, with the FTSE All-Share Index (FTSE All-Share) falling just 0.4% YTD. But as we cascade down the UK capitalisation spectrum away from the FTSE 100 realm, consistency in volatility and the returns profile diminishes.

The FTSE 250 (ex-ITs) Index (FTSE 250) has fallen 13% YTD amid these headwinds that we face, culminating in a significant period of relative underperformance vs the broader UK market. This now exceeds previous underperformance periods such as March 2020 (Covid-19), June 2016 (Brexit) and indeed 2008 (Global Financial Crisis). Notwithstanding these statistics, we believe that FTSE 250 investors should remain alert to the prospects that are now starting to present themselves considering the prevailing valuations and opportunities.

We believe that FTSE 250 investors should remain alert to the prospects that are now starting to present themselves considering the prevailing valuations and opportunities.

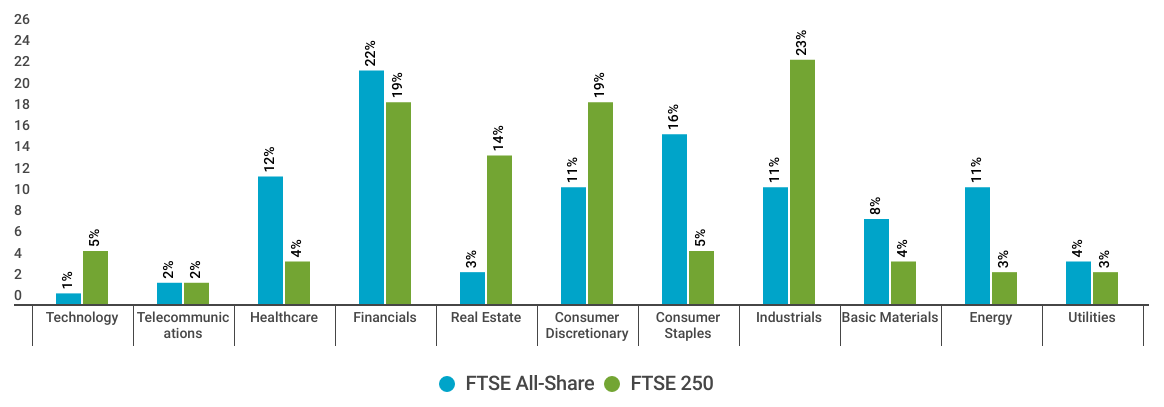

Underperformance vs the FTSE All-Share

Despite this YTD sell off and period of relative underperformance vs the broader market, we continue to believe that UK mid cap companies offer attractive opportunities. The sector profile of the FTSE 250 is materially distinct to that of the FTSE All-Share. The greater weighting to the domestic consumer and industrial companies has meant that the mid cap index has struggled to keep pace with blue chip indices YTD when encountered with soaring inflation, rallying oil and commodity prices and squeezed consumer budgets.

Also, with a higher weighting in the FTSE 250 to higher growth companies which have been out of favour YTD, it is no surprise to see the value oriented broad UK market outperform as forecasters predict an economic slowdown with interest rates, and consequently discount rates, rising as a result. Comparing to the FTSE All-Share which is 80% comprised of FTSE 100 companies, we find significantly higher weightings to value-oriented and relatively defensive sectors like oil and gas, mining, pharma and other safer havens which are assumed to fare well in inflationary and rising rate environments.

Source: FTSE Russell, as at 31 July 2022.

In spite of this sectoral disparity, we remain optimistic about the case for UK mid cap stocks where we believe that there is unique opportunity to leverage true, bottom-up investing. The FTSE All-Share is majority exposed to both lower growth companies and overseas earnings which means fluctuating currencies and the macro environment plays a much larger part in determining sector allocations and shorter-term returns. Compared to the FTSE 250, we have greater exposure to structural and niche growth businesses as well as a much larger investment universe from which to construct a diversified portfolio.

By focusing on the specific business characterises at a micro level there is a significant opportunity to add value through fundamental, bottom-up stock picking. This hands-on approach plunges us into the nuts and bolts of our investee companies. Enabling us to determine a valuation based on the business and end market characteristics, we find far less sensitivity to the fluctuating macroeconomic conditions that we’ve witnessed so far in 2022. Although there may be intermittent periods of underperformance when the prevailing macro backdrop is supportive of large cap valuations, one must remember the historic long-term outperformance of the FTSE 250 over the UK market.

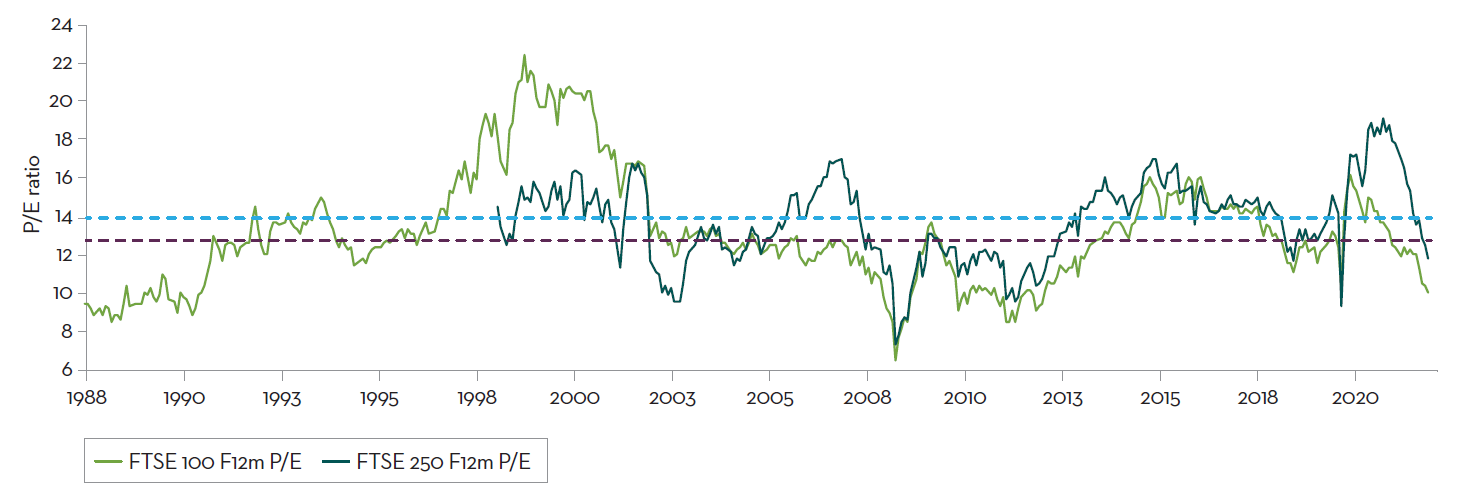

Valuations attractive

As with any period of underperformance, we view this as an opportunity to buy quality businesses at attractive valuations. As a result of the YTD sell off the FTSE 250 is now trading around 15-20% below its long term average, roughly 11.5x 12m forward price/earnings (P/E) compared with the long-term average of 13/14x P/E. Whilst it’s likely we’ll face a tougher trading environment in the short-term with increasing risks around corporate earnings through 2022 and into 2023, many stocks are now starting to price in an extremely pessimistic outlook for profits which we view as an enticing buying opportunity. This increasing ‘short-termism’ by many market participants disregards the long-term opportunities many companies face and overlooks those companies displaying more enduring growth prospects. There may be continued volatility throughout the remainder of 2022 as news flow and headlines portray a distinctly negative message, but our long-term horizon enables us to ride through these periods and reap the rewards once economic conditions become supportive of the FTSE 250.

Historic Price/Earnings ratio: FTSE 100 vs FTSE 250

Source: Barclays, as at 1 June 2022.

Corporates in good shape

Despite the reduced sentiment to mid cap stocks, we are of the opinion that many corporates are tackling the prevailing market challenges head on and have emerged from the global pandemic as better businesses – leaner, more agile, and with strong balance sheets. M&A activity in the mid cap space is also beginning to increase, with private equity and international businesses looking to capitalise on the attractive valuations supported by sterling’s recent weakness. If public markets are efficiently priced then the prospect of purchasing assets on attractive multiples is an opportunity for some but can also lead to quality companies being taken off of the market before their full value has been realised. Assessing the recent FTSE 250 M&A activity there has been little concentration within any specific sector. With additional healthy premiums we believe that this activity is very supportive of the mid cap index.

Recent bids in the index include Countryside Properties, Homeserve, Brewin Dolphin & Euromoney. With global private equity businesses sitting on some $3trn of dry powder ready to deploy, we would not be surprised to see further bids within the UK market. We are under no illusion that the entirety of this capital will all make its way onto UK shores however the £25bn of deals already announced in the UK YTD is an encouraging and supportive statistic. Furthermore, on the corporate front we are seeing a record year for share buybacks in the UK, reaching £33bn in value. Our mid cap portfolio has been a YTD beneficiary of this enhanced activity with companies such as Howden, Serco and Spectris all announcing buyback programmes.

The portfolio

Over the last 20 years the FTSE 250 index has generated annualised returns of around 10%, and our valuation modelling suggests that at current levels our portfolio is capable of producing a return in excess of this. We still observe above average return opportunities while factoring in a worsening profit environment even after the market rally in July. The portfolio is also yielding over 3% at current levels.

Our focus on valuation and quality fundamentals results in a preference for companies in robust capital positions, for example 57% of our portfolio has net cash on the balance sheet (excluding property companies). Such companies are starting from a position of relative strength and are best placed to grow both organically and inorganically through this challenging period we are faced with. Whilst the FTSE 250 does have more exposure to structural growth companies when compared to the broad market, we operate no intended style bias. This enables us to construct a balance between cyclical, growth and value names and has resulted in a period of strong relative performance against the direct peer group, some of whom are operating high conviction growth portfolios and are facing extreme performance challenges on an absolute and relative basis YTD.

Our valuation and risk discipline means that we have avoided the large derating witnessed in many highly rated stocks where valuations had departed from reality, and we remain cautious around paying high multiples for promises of future returns. We choose instead to focus on sensible priced opportunities and realistic near-term multiples. Although the FTSE 250 is majority domestic earning focussed, there is still a large portion of the index (c. 40%) where earnings are derived internationally. We do not see this as an opportunity to begin to make macro calls however we do recognise that this portion of the index is likely to benefit from tailwinds during a period of relative sterling weakness such as we have seen YTD.

Outlook & summary

We view the recent weakness as an attractive buying opportunity and this has enabled us to continue to add to existing names on share price weakness that we like such as QinetiQ, Spirent, and Pets at Home. Balance sheet strength remains a focus for us to maintain exposure to companies most likely to continue to invest, maintain their competitive advantage and exit this downturn in a strong position. As we saw during the pandemic period, opportunities arise to enhance one’s market position as weaker companies exit the market. We aim to invest with those firms who can capitalise on these opportunities and grow their market share.

We recognise the dynamic period we are now in, a complex and complicated phase that increases uncertainty. There are new economic and geopolitical challenges to face whilst entering a global slowdown as Central Banks grapple with inflationary pressures. But through the uncertainty we will not diverge from our tried and tested process, that is focussing on valuation and business and industry fundamentals.

Whilst the macro signals are not clear cut at the moment, one thing is – many companies have taken a huge step forward in the past 2 years. This has instilled a degree of resilience and strength in many businesses. This should not be understated as we believe many of our companies are in a position of strength, both financially and competitively to weather this slowdown and emerge in a much better position. In times like this it is crucial to partner with experienced and skilled management teams, those with a combination of both competent operational execution combined with bigger picture strategic thinking,

We will look to use this volatility and dislocation between share price and value to our advantage as we believe that long term UK Mid cap return opportunities are increasingly enticing.

Source: Bloomberg, 31 July 2022 unless otherwise stated. YTD as at 31 July 2022.

Important information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

This document may not be distributed to third parties. It is confidential and intended only for the recipient. The recipient may not photocopy, transmit or otherwise share this [document], or any part of it, with any other person without the express written permission of Martin Currie Investment Management Limited.

This document is intended only for a wholesale, institutional or otherwise professional audience. Martin Currie Investment Management Limited does not intend for this document to be issued to any other audience and it should not be made available to any person who does not meet this criteria. Martin Currie accepts no responsibility for dissemination of this document to a person who does not fit this criteria.

Some of the information provided in this document has been compiled using data from a representative account. This account has been chosen on the basis it is an existing account managed by Martin Currie, within the strategy referred to in this document. Representative accounts for each strategy have been chosen on the basis that they are the longest running account for the strategy. This data has been provided as an illustration only, the figures should not be relied upon as an indication of future performance. The data provided for this account may be different to other accounts following the same strategy. The information should not be considered as comprehensive and additional information and disclosure should be sought.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

The information provided should not be considered a recommendation to purchase or sell any particular strategy / fund / security. It should not be assumed that any of the securities discussed here were or will prove to be profitable.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile

Martin Currie Investment Management Limited, registered in Scotland (no SC066107), Saltire Court, 20 Castle Terrace, Edinburgh EH1 2ES. Authorised and regulated by the Financial Conduct Authority. Tel: 44 (0) 131 229 5252 Fax: 44 (0) 131 228 5959 www.martincurrie.com. Please note that calls to the above number and any other communications may be recorded.

© 2022 Martin Currie Investment Management Limited