Content navigation

Executive Summary

- In this report, we focus on two aspects. Firstly, how we approach investing in technology in line with our investment philosophy, and how that manifests itself into companies in the portfolio within the Technology, Media and Telecommunications (TMT) space, and more broadly. Secondly we discuss the effects of Artificial Intelligence (AI) on the TMT landscape and the areas we are focusing on.

- We believe that taking a long-term approach and focusing on companies with strong balance sheets and sustainable business models, which are operating in attractive industry dynamics, facing long term structural growth opportunities, with resilient earnings and pricing power remains the right approach in our view. The combination of improved products and services, with faster adoption rates and differentiation versus lagging competitors makes AI a significant secular opportunity for quality growth companies across sectors in a similar way to globalisation and the internet.

- Our global portfolio has significant exposure to companies with high exposure to AI, at c.30% of the portfolio. Holdings include ASML, Nvidia, Microsoft, Adobe and Atlas Copco.

Source: Martin Currie as at 30 September 2023. Data presented is for the Martin Currie Global Long-Term Unconstrained representative account.

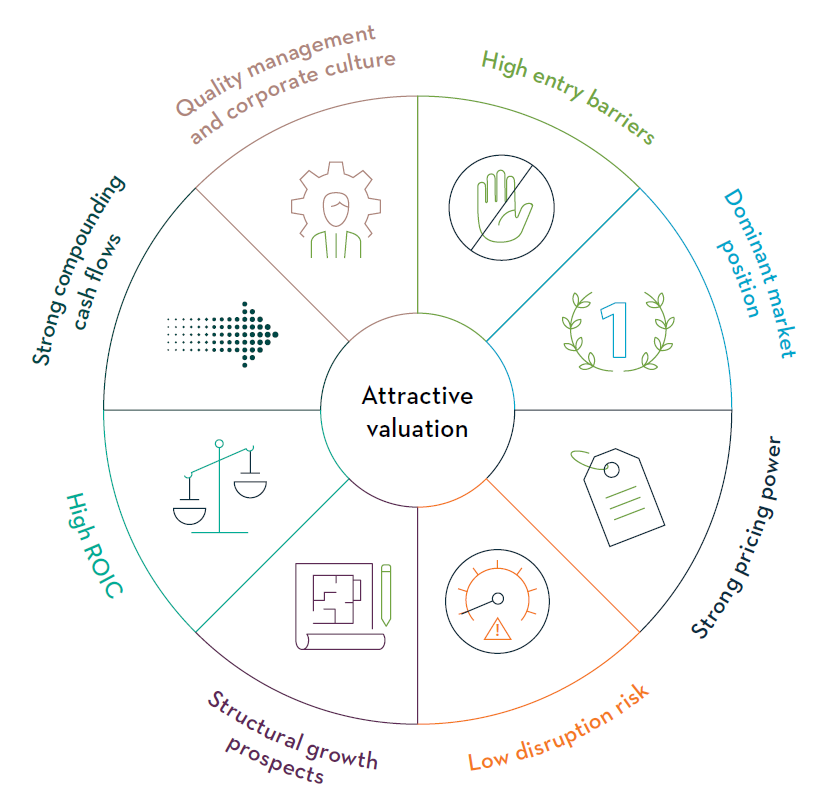

Sustainable quality growth companies in the technology sector

Combining strong industry, financial and governance attributes at the right valuation

At its heart, the Global Long-Term Unconstrained (GLTU) investment philosophy looks for companies with high returns on invested capital (ROIC) and attractive growth prospects. The process is the same across sectors with a focus on high barriers to entry and, dominant market positions with structural growth prospects

Technology companies are well placed to access opportunities for higher ROIC as they are relatively capital-light at scale. Typically, this means that barriers to entry are tied to intellectual capital rather than the amount of dollars spent. Technology companies also benefit from product innovation being more iterative and there being significant benefits from scale through network effects.

These end up being companies with a structural ability to maintain their competitive advantages, precisely because of the scale advantage that they have built. Examples include Nvidia, where the company has built the largest developer ecosystems around its AI software platform, CUDA. As more developers use the platform, they also create content which improves the offering, thereby creating a virtuous cycle. Individual engineers with extremely limited time simply want the best tools and are unlikely to adopt other tools as a result.

Similar commentary can be made for other technology holdings which we believe to have significant scale advantages. ASML has 100% share in the leading-edge lithography process, where it simply is not attractive economically to create a direct competitor. In addition, the task would come with extremely high complexity and domain expertise across an extended value chain that ASML has collaborated with for decades. Adobe has become the industry software for digital designers to use, while Microsoft similarly benefits from developers on its cloud ecosystem and global distribution scale.

Taking a step back, the areas we tend to find harder to gain conviction are Media and Telecoms. For the former we see execution risk in creating superior content, such as a new hit movie or video game. In addition, the barriers to entry for content creation is crumbling from established companies to user-generated content. We believe this could be accelerated by AI-generated content.

Furthermore, media is an area where “big tech” has a strategic interest, from Amazon’s Prime platform to Microsoft’s Xbox and Apple’s Music and TV to name a few. We believe Telco’s are largely regulated utilities and therefore suffer from a range-bound level of ROIC. In addition, we tend to steer away from areas where disruptive capital is extremely intensive and therefore we periodically monitor which areas Venture Capital funding is being channelled into, to assess the new entrant risk over a longer time frame. In such a vibrant sector, areas which are not facing significant disruption risk, and therefore that do not evolve too rapidly, can yield extremely value accretive business models.

-

Technology companies are well placed to access opportunities for higher ROIC as they are relatively capital light at scale. Typically, this means that barriers to entry are tied to intellectual capital rather than the amount of dollars spent.

Implications of AI

Portfolio analytics – Thematics

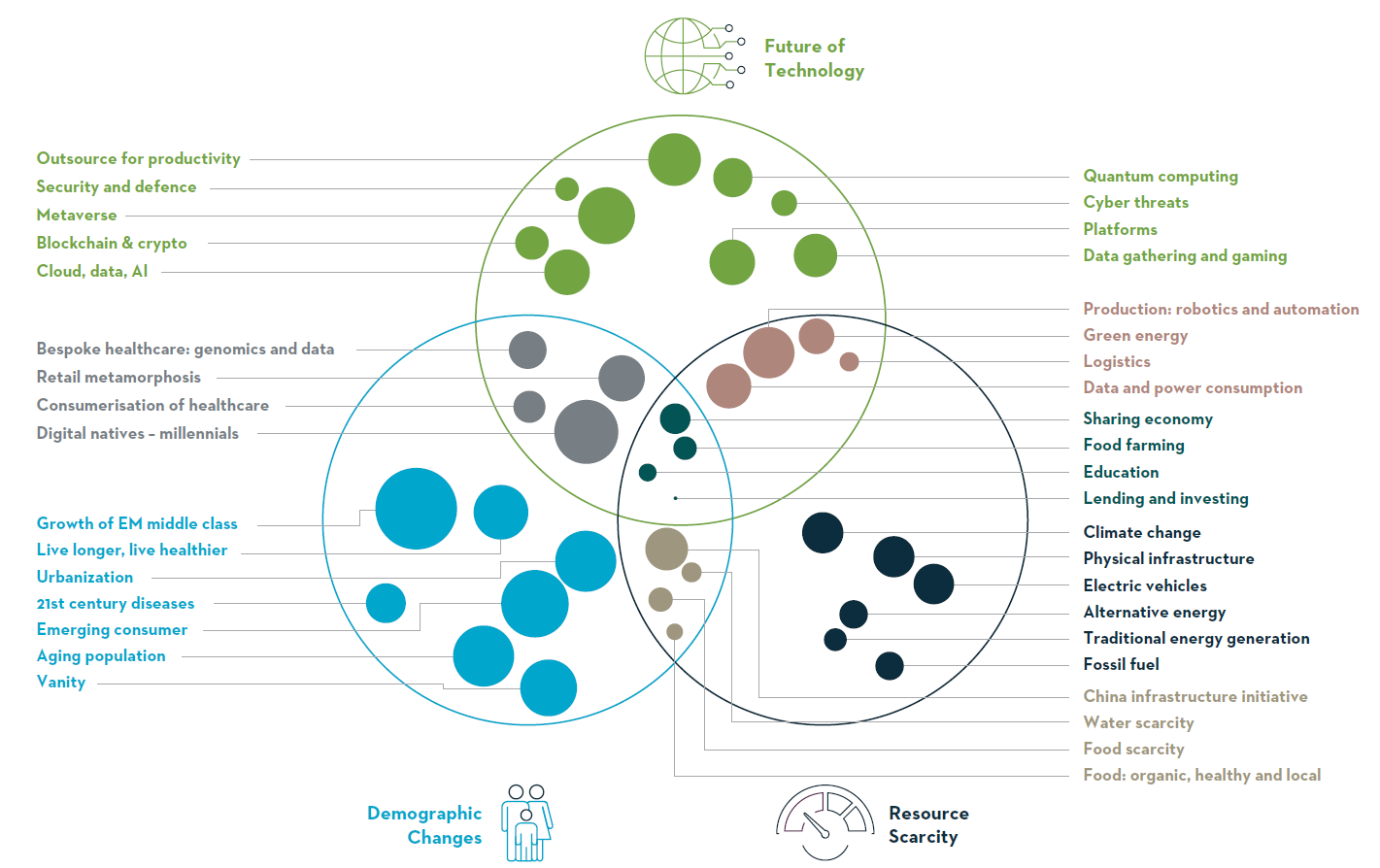

A challenge companies with high ROIC can face is a lack of growth opportunities. As mentioned, one attractive side of Technology companies is that they usually have secular demand drivers which outgrow the global economy. Within our proprietary thematics framework comprising our three mega-trends, we would specifically highlight key themes such as: Cloud & AI, Data Gathering, Digital Natives, Platforms, Metaverse, and Blockchain.

Source: Martin Currie and FactSet as at 30 June 2023. Data presented is for the Martin Currie Global Long-Term Unconstrained representative account.

AI has been one of the dominant, if not the dominant, topics of the year. As we reflect on our Thematics framework, we find AI to be highly synergistic with the other themes. For example, the AI and data gathering both improve the value of each other. The more data you have the better the AI models, and AI can be used to harness real world events into recordable data. We see the Metaverse as being in its early stages with multiple related themes being key enablers such as Cloud & AI, Digital Natives, Platforms and Blockchain. As an example, recent developments in AI significantly advances our ability to build AI “agents” or interactive characters to create much more immersive digital experience.

Implications of AI for corporates and investing

We believe taking a long-term approach and focusing on companies with strong balance sheets and sustainable business models, which are operating in attractive industry dynamics, facing long term structural growth opportunities, with resilient earnings and pricing power remains the right approach.

The combination of improved products and services, with faster adoption rates and differentiation versus lagging competitors makes AI a significant secular opportunity for quality growth companies across sectors in a similar way to globalisation and the internet. The portfolio has significant exposure to companies with high exposure to AI, at c.30% of the portfolio. Holdings include ASML, Nvidia, Microsoft, Adobe and Atlas Copco.

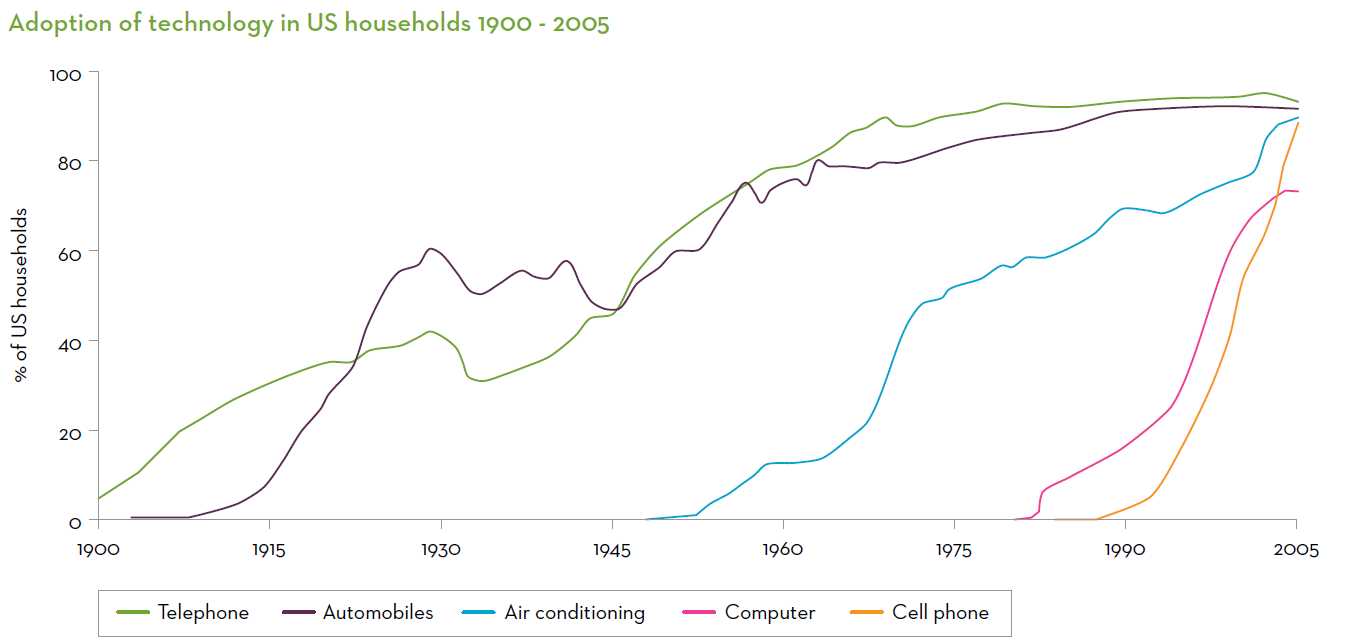

Adoption cycles are accelerating

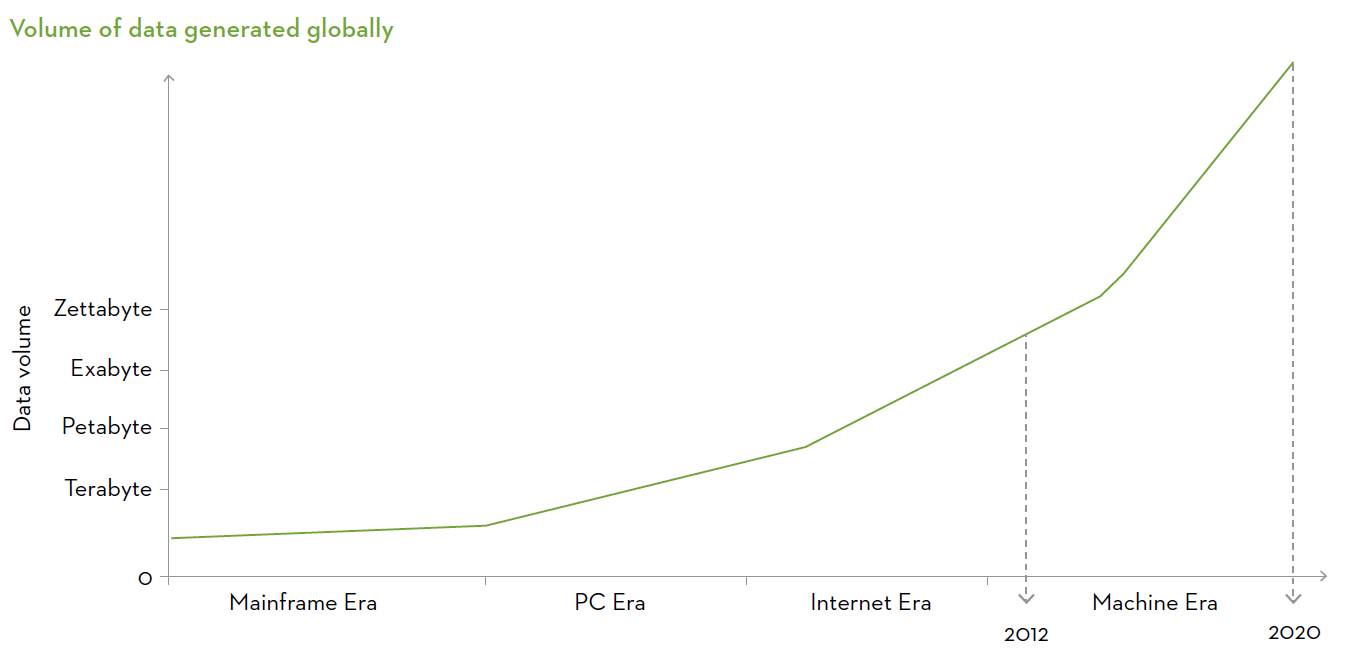

The confluence of technologies being synergistic with each other. Two key historical trends have been extremely impactful to the world over the period. The internet era and globalisation has driven long term secular opportunities for industry leaders to win at the global scale. The processing resource advances in the PC industry combined with connectivity led to the smartphone. Data creation has accelerated as we have become more interconnected.

Source: Harvard Business Review and The New York Times. https://hbr.org/2013/11/the-pace-of-technology-adoption-is-speeding-up

Originally published 25 November 2013, updated 25 September 2019.

AI technologies have the potential for exponential adoption

Up to now, adoption cycles have been largely limited by humans and the way we behave. The number of machines can grow much more rapidly, meaning they can adopt new technologies and processes more quickly. Going forward we expect most data to be ingested and created by machines. Machines can scale significantly faster than humans; for example the International Data Corporation (IDC) estimates that there will be 41.6bn IoT (Internet of Things) devices, capable of generating 79.4 zettabytes of data. This is simply far beyond humans' ability to process so we will increasingly rely on machine-to-machine communication and artificial intelligence to process the information. Large Language Models such as Chat-GPT are being trained on volumes of data, and each has been increasing the size of the model by 10x, typically per year.

Source: Martin Currie and Alation. https://www.alation.com/blog/first-pillar-of-data-culture-data-search-discovery

As at 9 June 2021.

Characteristics of AI leaders

Taking a closer look at AI, a company's ability to create a leadership position in AI will be centered on three critical areas: Computing Power, Talent, and Proprietary Data. Differentiation in Computing Power is primarily driven by scale given the extremely large compute requirements which continue to grow at a rapid pace (10x per year). We are not surprised that the leading models have come from Microsoft (Open-AI), Alphabet and Meta (Facebook). The second element is Talent. There has been a tremendous war over talent with notable teams moving between large companies. Meta, for example, has had over half of the 19 authors of an AI paper written in May 2022 leave the company. Finally, proprietary data will become an increasingly important differentiator and favour the incumbents who can manage the AI transition and incorporate the technology into new products and services.

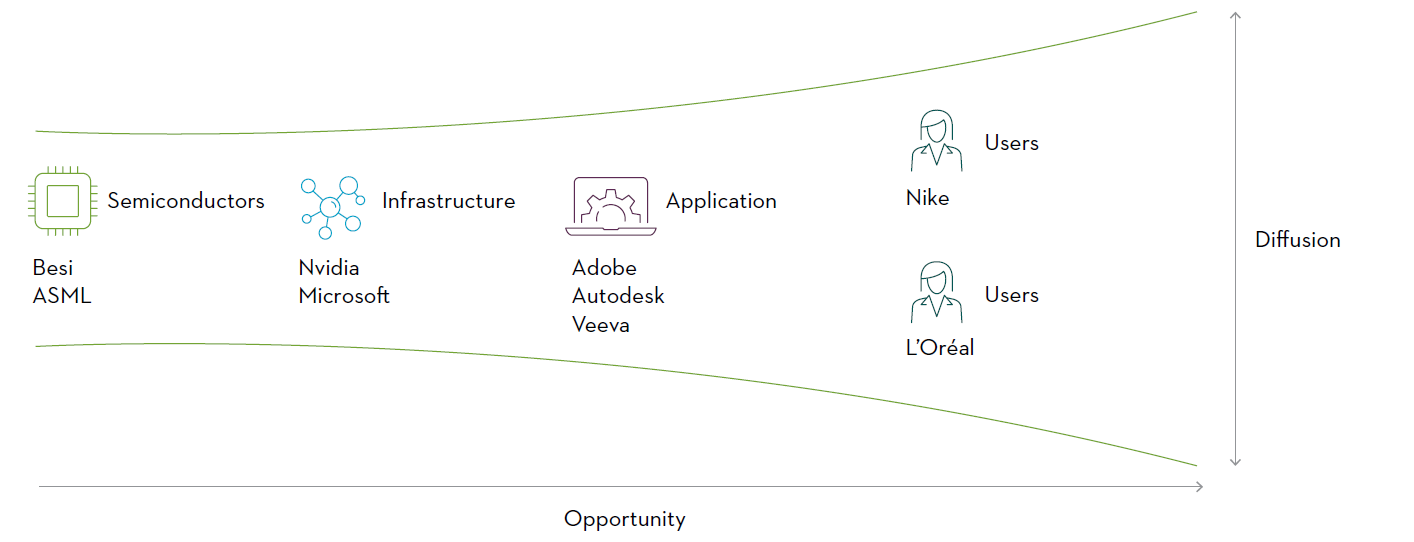

AI Value Chain

The opportunities within AI follow through to the technology landscape and expand into downstream industries. Taking a look at the value-chain in more detail, AI is extremely computing power intensive. This will drive incremental semiconductor requirements going forward, benefiting leading companies such as ASML. Nvidia supports the industry by developing semiconductors into useful products where software is needed to successfully accelerate the computation. Many AI models will need to be deployed, industrialised and scaled globally, which is where Microsoft’s cloud offering is of notable value. Software companies such as Adobe can look to incorporate AI to develop improved tools to increase productivity to its customers. Adobe has released its product “Firefly” which incorporates generative AI to speed up and improve digital design. As with globalisation and the internet, we believe AI gives industry leaders the opportunity to improve their products to end customers. For example, Nike has mentioned that it is using Adobe’s Firefly to bring greater user personalisation to its mobile app.

A seismic shift

All in all, we believe that AI brings a seismic shift in terms of potential across all areas of the economy. It will permit corporates to enhance their productivity and/or creativity, and to either achieve, maintain, or increase their competitive positioning within the industries in which they operate. This means companies that do not use AI will be at greater risk of being outcompeted by competitors using AI. Therefore it makes it critical for corporates to embrace AI, as an important area both in terms of strategic and military investment opportunity. As well as in terms of assessing the adequate regulatory framework that will need to be applied, to ensure an ethical use of the technology. There will be plenty more focus in this area, as we continue to seek investment opportunities as long-term investors, so we will update our readers periodically about this important part of our portfolios.

The information provided should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the security transactions discussed here were, or will prove to be, profitable.

Important Information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.

- Emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. Accordingly, investment in emerging markets is generally characterised by higher levels of risk than investment in fully developed markets.

- The strategy may invest in derivatives Index futures and FX forwards to obtain, increase or reduce exposure to underlying assets. The use of derivatives may result in greater fluctuations of returns due to the value of the derivative not moving in line with the underlying asset. Certain types of derivatives can be difficult to purchase or sell in certain market conditions.

For wholesale investors in Australia:

This material is provided on the basis that you are a wholesale client. MCIM has entered an Intermediary arrangement with Franklin Templeton Australia Limited (ABN 76 004 835 849) (AFSL No. 240827) (FTAL) to facilitate the provision of financial services by MCIM to wholesale investors in Australia. Franklin Templeton Australia Limited is part of Franklin Resources, Inc., and holds an Australian Financial Services Licence (AFSL No. AFSL240827) issued pursuant to the Corporations Act 2001.

For professional investors in Canada.

This material is intended for residents in, or incorporated in, Canada and are a Permitted Client for the purposes of MI 31-103. The information on this section of the website is not intended for use by any other person, including members of the public.

Martin Currie Inc, incorporated in New York with its registered office at 280 Park Avenue, New York, NY 10017 and having a UK branch registered in Scotland (no SF000300), Head office, 5 Morrison Street, 2nd floor, Edinburgh, EH3 8BH, Tel: +44 (0) 131 229 5252 Fax: +44 (0) 131 222 2532 www.martincurrie.com, operates under the International Adviser Exemption with the Ontario Securities Commission (‘OSC’) and is therefore currently not required to be registered as a portfolio manager for the purposes of MI 31-103. Martin Currie Inc. is also authorised by the UK Financial Conduct Authority.

For the avoidance of doubt, nothing excludes, limits or restricts our obligations to you under the UK Financial Services and Market Act 2000, National Instruments or any other applicable law or regulation.

The opinions and views in this website do not take into account your individual circumstances, objectives, or needs and are not intended to be recommendations of particular financial instruments or strategies to you.

This website does not identify all the risks (direct or indirect) or other considerations which might be material to you when entering any financial transaction. You should consult with your professional advisers before undertaking any investment activity. The information provided on this website should not be treated as advice or a recommendation to buy or sell any particular security or other investment. The information on this website has not been reviewed by any competent regulatory authority.

For professional investors:

In the People’s Republic of China:

This document does not constitute a public offer of the strategy, whether by sale or subscription, in the People’s Republic of China (the “PRC”). These strategies are not being offered or sold directly or indirectly in the PRC to or for the benefit of, legal or natural persons of the PRC.

Further, no legal or natural persons of the PRC may directly or indirectly purchase any of the strategy or any beneficial interest therein without obtaining all prior PRC’s governmental approvals that are required, whether statutorily or otherwise. Persons who come into possession of this document are required by the issuer and its representatives to observe these restrictions.

In Hong Kong:

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

In South Korea:

This document is for information purposes only. It is prepared and presented to provide an introduction to the business of MCIM and its related companies (collectively known as ‘Martin Currie’). This document does not constitute an offer to sell or a solicitation of any offer to invest in any security, fund or other vehicle managed or advised by Martin Currie.

None of the security(ies), fund(s) or vehicle(s) managed by or advised by Martin Currie are registered in South Korea under the Financial Investment Services and Capital Markets Act of Korea and accordingly, none of these instruments nor any interest therein may be offered, sold or delivered, or offered or sold to any person for re-offering or resale, directly or indirectly, in South Korea or to any resident of South Korea except pursuant to applicable laws and regulations of South Korea.

Martin Currie is not registered with or regulated by any regulatory authorities in South Korea.