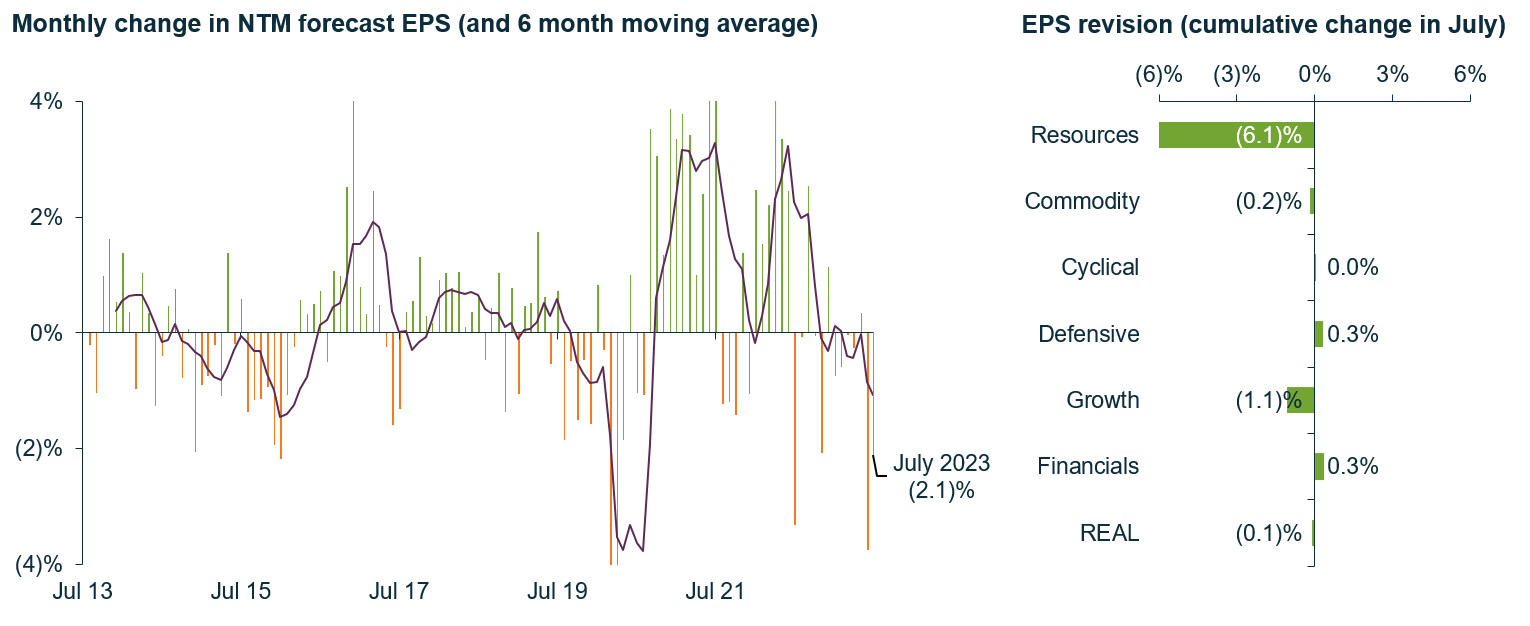

Heading into this reporting season, we are concerned to see that the market is forecasting significant earnings per share (EPS) downgrades, despite continuing strong economic data for Australia.

Resources dominate negative revisions

While the company reporting season officially falls in the month August, of the ~30 companies that have announced quarterlies or trading updates in July so far, there has been a substantial negative EPS revision skew.

What is most surprising to us, given concerns about interest rate impacts on consumers, is that the negative revisions have been mostly concentrated in the Resources space.

Source: Martin Currie Australia, FactSet; as of 31 July 2023. Data for the S&P/ASX 200 Index. NTM: next twelve months

Share prices disconnect from earnings fundamentals

Rather than the Resource company results themselves (as the start of the deteriorating revisions pre-date the latest round of quarterlies), the weak outlook for China property policy appears to be a key force for the downgrades. The impact of lower forward commodity price expectations is feeding into weaker EPS expectations.

However, there are several conflicting forces impacting the outlook for Resource stocks in each direction. These include:

- very poor growth data for Chinese property;

- impending steel production tightening in the second half;

- strong steel production being driven by exports;

- a perceived large number of short positions in commodity stocks; and

- hopes that stimulus is about to arrive.

| Negative drivers | Positive drivers |

|---|---|

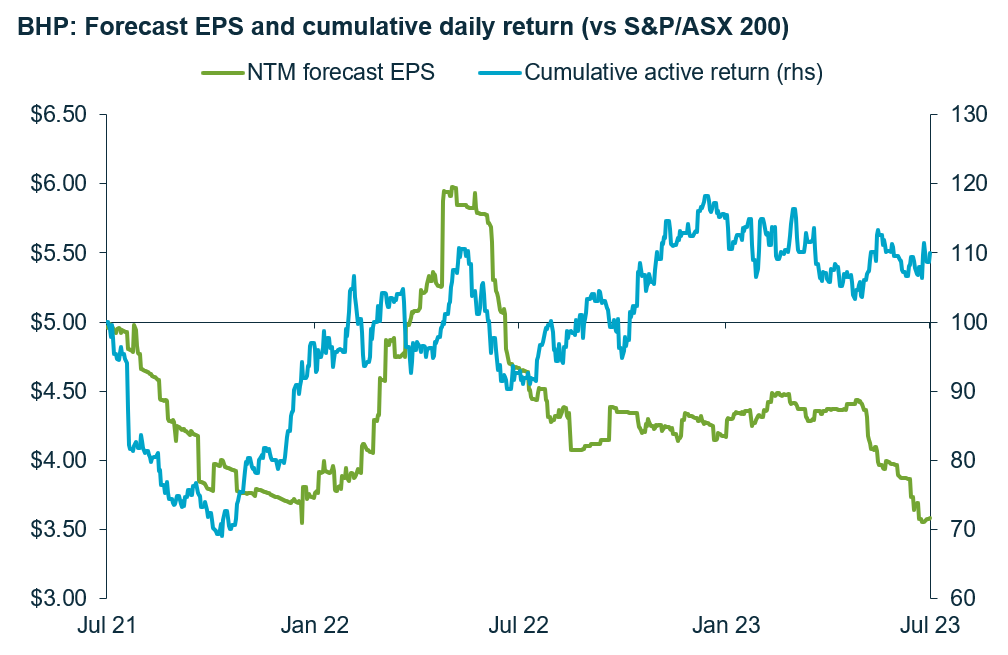

Conflicting drivers have created a real disconnect between EPS revisions and company share prices. Earnings outlooks appear to be driven by the fundamentals, whereas stock prices are being driven mainly by the China stimulus hope.

This is illustrated well by the recent divergence in BHP Group’s consensus EPS and share price in the chart below.

Source: Martin Currie Australia, FactSet; as of 31 July 2023. NTM: next twelve months

Weaker domestic economic expectations to dominate non-resource outlook

The miners have dominated the discussion in the lead-in to reporting season proper. However, Resource quarterlies have not generally been a reliable predictor of overall reporting season outcomes. We track overall outcomes in terms of ‘Surprise’, ‘Revisions’, and ‘Price Reaction’ for the S&P/ASX 200.

In contrast to the Resource downgrades, we are seeing lead-in EPS revisions for the Industrials, Financial and Real Asset sectors being broadly flat. This, and the general lack of profit warnings, suggests that the reporting season could be more balanced overall.

However, our February reporting season theme was “looking over the edge”, and the Australian market continues to stand on a mortgage rate cliff and a potential recession. The August results will likely be dominated by cautious views on the consumer, costs and future EPS guidance, rather than any significant jubilation for the robust earnings delivered in the last six months.

Heading into this reporting season, we are concerned to see that the market is forecasting significant earnings per share (EPS) downgrades, despite continuing strong economic data for Australia.

Resources dominate negative revisions

While the company reporting season officially falls in the month August, of the ~30 companies that have announced quarterlies or trading updates in July so far, there has been a substantial negative EPS revision skew.

What is most surprising to us, given concerns about interest rate impacts on consumers, is that the negative revisions have been mostly concentrated in the Resources space.

Source: Martin Currie Australia, FactSet; as of 31 July 2023. Data for the S&P/ASX 200 Index. NTM: next twelve months

Share prices disconnect from earnings fundamentals

Rather than the Resource company results themselves (as the start of the deteriorating revisions pre-date the latest round of quarterlies), the weak outlook for China property policy appears to be a key force for the downgrades. The impact of lower forward commodity price expectations is feeding into weaker EPS expectations.

However, there are several conflicting forces impacting the outlook for Resource stocks in each direction. These include:

- very poor growth data for Chinese property;

- impending steel production tightening in the second half;

- strong steel production being driven by exports;

- a perceived large number of short positions in commodity stocks; and

- hopes that stimulus is about to arrive.

| Negative drivers | Positive drivers |

|---|---|

Conflicting drivers have created a real disconnect between EPS revisions and company share prices. Earnings outlooks appear to be driven by the fundamentals, whereas stock prices are being driven mainly by the China stimulus hope.

This is illustrated well by the recent divergence in BHP Group’s consensus EPS and share price in the chart below.

Source: Martin Currie Australia, FactSet; as of 31 July 2023. NTM: next twelve months

Weaker domestic economic expectations to dominate non-resource outlook

The miners have dominated the discussion in the lead-in to reporting season proper. However, Resource quarterlies have not generally been a reliable predictor of overall reporting season outcomes. We track overall outcomes in terms of ‘Surprise’, ‘Revisions’, and ‘Price Reaction’ for the S&P/ASX 200.

In contrast to the Resource downgrades, we are seeing lead-in EPS revisions for the Industrials, Financial and Real Asset sectors being broadly flat. This, and the general lack of profit warnings, suggests that the reporting season could be more balanced overall.

However, our February reporting season theme was “looking over the edge”, and the Australian market continues to stand on a mortgage rate cliff and a potential recession. The August results will likely be dominated by cautious views on the consumer, costs and future EPS guidance, rather than any significant jubilation for the robust earnings delivered in the last six months.

REPORTING SEASON WRAP: Surviving the profit downturn

As we enter this contractionary economic environment, it is critical for investors to be discerning in their stock picking. The Australian reporting season will help reveal critical signals and fundamental information to provide the clues all investors need to position their portfolios to be resilient to headwinds. For active investors like Martin Currie Australia (MCA), these periods are extremely significant in shaping assessments of forward-looking value and sustainable dividends for Australian companies.

Register here for an exclusive Reporting Season Wrap webinar on Tuesday, 5 September at 11am. The discussion will cover the major themes and drivers affecting company results, and MCA’s outlook for what it all means for investors in Australian Equities.

In late September, we will also publish our semi-annual Reporting Season Wrap, which will bring together our full statistical framework, and key fundamental views and insights from company engagement.

-

The August results will likely be dominated by cautious views on the consumer, costs and future EPS guidance, rather than any significant jubilation for the robust earnings delivered in the last six months.

Chart disclaimers

Past performance is not a guide to future returns.Source: Martin Currie Australia, FactSet; as of 31 July 2023.

Expected next 12 Months (NTM) data is calculated using the weighted average of broker consensus forecasts of each portfolio holding – because of this, the returns quoted are estimated figures and are therefore not guaranteed and may differ materially from the figures mentioned. The figures may also be affected by inaccurate assumptions or by known or unknown risks and uncertainties. In respect of the broker consensus data the number of brokers included for each individual stock will depending on active coverage of that stock by a broker at any point in time. A median of brokers is typically utilised. All estimates avoid stale forecasts which are removed after a certain number of days. The information provided should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the security transactions discussed here were, or will prove to be, profitable.

Important information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

The information provided should not be considered a recommendation to purchase or sell any particular strategy/ fund/security. It should not be assumed that any of the security transactions discussed here were or will prove to be profitable.

It is not known whether the stocks mentioned will feature in any future portfolios managed by Martin Currie. Any stock examples will represent a small part of a portfolio and are used purely to demonstrate our investment style.

Chart disclaimers

Past performance is not a guide to future returns.Source: Martin Currie Australia, FactSet; as of 31 July 2023.

Expected next 12 Months (NTM) data is calculated using the weighted average of broker consensus forecasts of each portfolio holding – because of this, the returns quoted are estimated figures and are therefore not guaranteed and may differ materially from the figures mentioned. The figures may also be affected by inaccurate assumptions or by known or unknown risks and uncertainties. In respect of the broker consensus data the number of brokers included for each individual stock will depending on active coverage of that stock by a broker at any point in time. A median of brokers is typically utilised. All estimates avoid stale forecasts which are removed after a certain number of days. The information provided should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the security transactions discussed here were, or will prove to be, profitable.

Important information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

The information provided should not be considered a recommendation to purchase or sell any particular strategy/ fund/security. It should not be assumed that any of the security transactions discussed here were or will prove to be profitable.

It is not known whether the stocks mentioned will feature in any future portfolios managed by Martin Currie. Any stock examples will represent a small part of a portfolio and are used purely to demonstrate our investment style.