Content navigation

As 2024 approaches, British politicians are eyeing the calendar with a mixture of excitement and fear.

Recently we have witnessed around a third of all MPs standing down, significant boundary revisions and the most solid lead for Labour since 1996 and the subsequent Tony Blair landslide of 1997.

What can we look forward to in the market? Has the market already discounted any impact?

Firstly, and much to the irritation of pollsters, most people only make up their minds to vote a few days before the election date. The British public has been voting with a lower turnout since the peak in 19921. That suggests that there is still room for a surprise. And with improving economic news that inflation is falling sharply and growth is resuming, those MPs in vulnerable seats may yet survive.

-

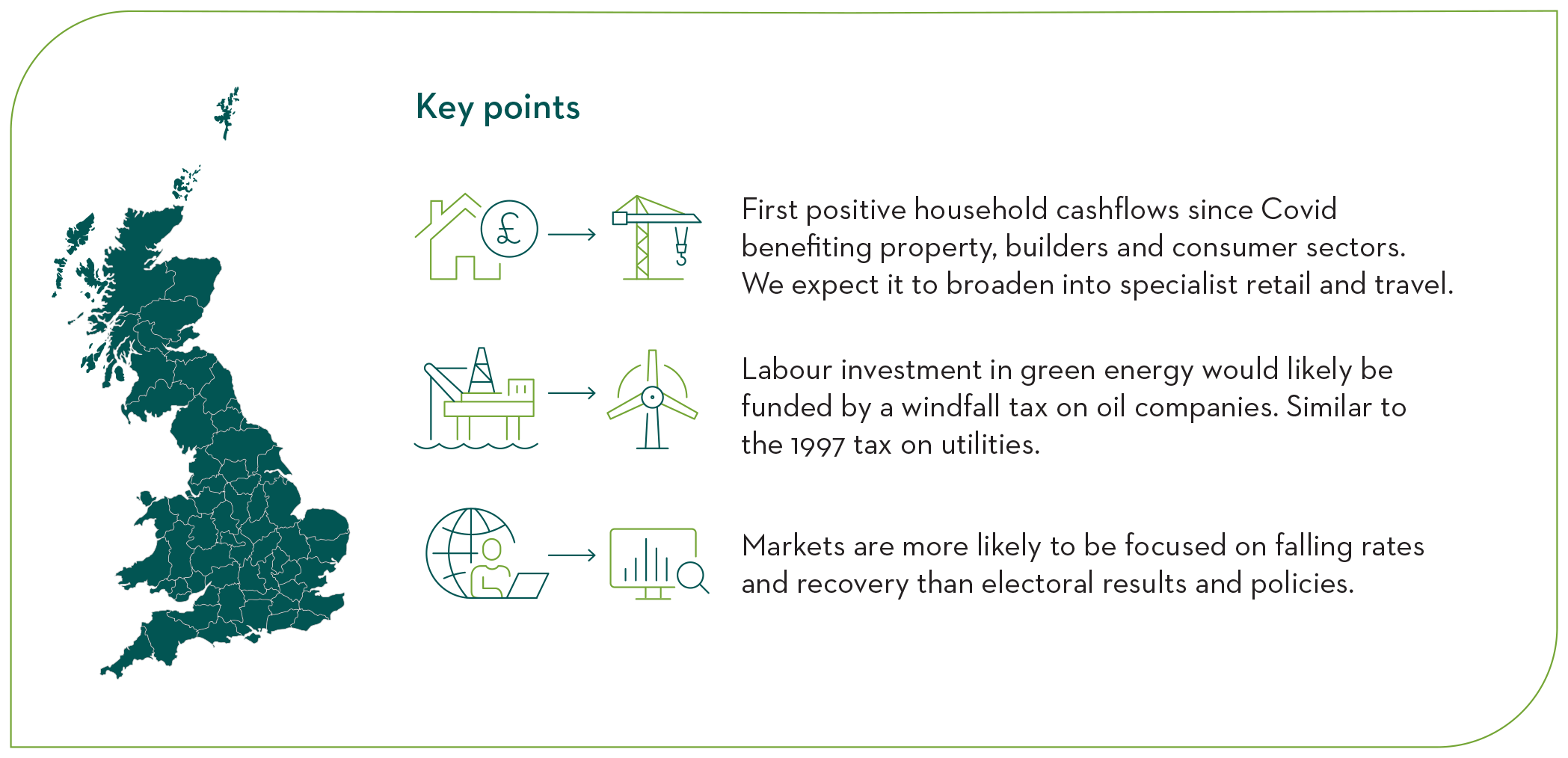

With rates potentially falling as well, it is the recovery sectors of property, builders and consumers that are driving the rally already upon us. Expect this to broaden, taking in more of the consumer stocks from specialist retailers to holidays.

Consumer stocks positioned to benefit from recovery

But the economic policies of the two main protagonists, the incumbent Conservative Party and re-surgent Labour party are closer than they have been since 2010. Rising interest rates, high post-Covid debt are the key drivers while the lessons of Liz Truss’s brief and disastrous dash for growth are all too fresh in the memory.

But with growth in real wages in 2024 and a meaningful tax cut (National Insurance) the economy will start to grow again. Driven by positive household cash flows for the first time since the end of the Covid lockdown2.

With rates potentially falling as well, it is the recovery sectors of property, builders and consumers that are driving the rally already upon us. Expect this to broaden, taking in more of the consumer stocks from specialist retailers to holidays.

Windfall taxes and investment in renewables?

Could this continue post election? Probably, but by then the rally heralding the new recovery will be well under way. There is certainly a focus on building out renewable energy from the Labour party, but how to fund that without tax rises from consumers or corporates. This is not unlike the “windfall tax” that Gordon Brown introduced on the utilities in 1997.

In fact, it is worth remembering that he also cut corporation tax and capital allowance. The markets liked that first budget, with the independence of the Bank of England, the UK pound, weak before the election, rallied. The UK gilt market had an excellent year as yields that were 7.5% at the start of the year fell sharply after to 6.2%3.

Gordon Brown’s first budget in July 1997 featured cuts in corporation tax, increased incentives for companies to invest and a windfall tax on utilities. Rachel Reeve who is expected to be Labour’s first Chancellor of the Exchequer since 2010 in her speech to the Labour party, promised fiscal probity, a windfall tax on oil companies, and investment in green energy.

Interestingly, the utility sector which was hit by the “windfall tax” in 1997 rallied sharply after the election, having been subdued before it4.

Buying in UK favours lower inflation and the consumer sector

How will the Bank of England, in their role as the only economic restraining force, react to growth in 2024? They will continue to be “data dependent” and with three members of the Monetary Policy Committee (MPC) still voting for a rise, there is still a big split.

But with the rest of Europe mired in contraction, and few signs of it ending, inflationary pressures are ebbing away. It is clear that supply chains are now properly repaired in the post Covid period.

Put simply what cannot be sold in Europe will be sold in the UK, in particular building materials. Again, all this favours lower inflation and the consumer sectors.

Rates and recovery to dominate not elections and policy

So oddly, with a major reversion in electoral fortunes from 2019’s Conservative majority in the offing, the market may not have much to worry about. Falling rates and recovery are going to dominate the economic and market news, not elections and policy speeches.

Blair and Brown were fortunate to inherit a decent economy in 1997 and chose to tread carefully. (Sir Keir) Starmer and Reeve may be equally lucky. They are certainly treading the path of their predecessors.

Sources

1Source: Statista, House of Commons; BBC, Turnout at elections. December 2019.

2Source: Office for National Statistics, December 2023.

3Source: Source: Bank of England – Quarterly bulletin – February 1998.

4Source: Morningstar. UK sector 12 month performance from 1 January 1997 - 31 December 1997.

Important Information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’). It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the named manager as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

The analysis of Environmental, Social and Governance (ESG) factors forms an important part of the investment process and helps inform investment decisions. The strategy/ies do not necessarily target particular sustainability outcomes.

Risk warnings - Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.’

- Income strategy charges are deducted from capital. Because of this, the level of income may be higher but the growth potential of the capital value of the investment may be reduced.